The repercussions of the subprime crisis on real estate prices in the United States, along with the ever-increasing real estate prices in Israel, have made the American market a hub for real estate investments by many Israelis. The Bank of Israel estimates that approximately 3 billion NIS was invested by Israelis in the United States in 2020.

Have you considered investing in real estate in the United States? If so, it is important to take tax considerations into account early in the process of evaluating each investment opportunity and to develop a tax plan that suits your needs. As with any investment, tax implications and planning are critical to ensuring profitability. These factors can determine whether an investment becomes a great success or a financial failure.

This is especially true for real estate investments in the United States, which are subject to multiple taxation levels: federal tax, state tax (applicable based on the state in which the property is located), municipal tax, estate tax, branch tax, and Israeli income tax. Additionally, other taxes may apply depending on the specifics of the investment. Lack of familiarity with the complex American tax system, which includes tens of thousands of regulations, could put your investment at risk.

In this article, we will not address state and municipal taxes (important as they may be) but will focus specifically on federal income tax, estate tax, branch tax, and Israeli income tax. We will examine the various taxation routes while reviewing the alternative structures available to investors.

Choosing the Right Investment Structure

The importance of making an informed decision about how to structure your investment is well known. The way the investment is organized and the ownership structure of the property will determine the applicable tax burden. Different tax regulations apply to individuals, foreign companies, and local companies. Proper tax planning will analyze these differences to determine the most profitable structure for the investor.

Possible Investment Structures

Investing as an Individual

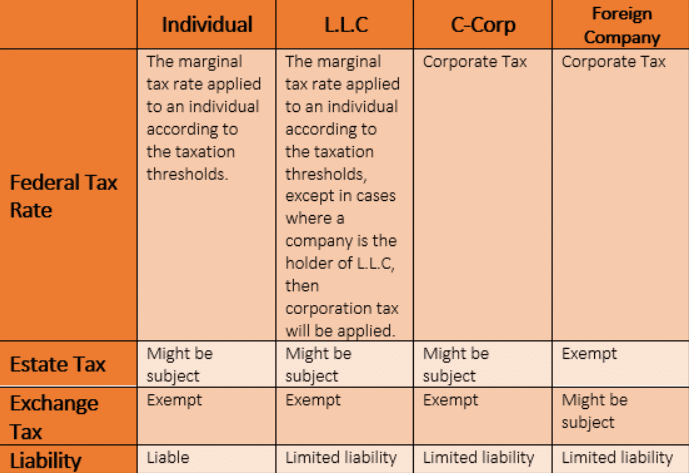

When purchasing real estate directly, the buyer is a private individual who owns the property personally. An investor who is not a U.S. citizen will be required to file a tax return with the Internal Revenue Service (IRS) using Form 1040NR.

This investment structure avoids company formation fees and complex reporting requirements, reducing administrative costs that could otherwise impact profitability. Additionally, individual investors benefit from lower tax rates compared to corporations.

However, investing as an individual comes with drawbacks. First, the investor may be subject to U.S. estate tax. Second, unlike corporate structures, an individual does not benefit from limited liability protection—meaning personal assets could be exposed to claims or lawsuits.

Investing through an LLC (Limited Liability Company)

Establishing a limited liability company (LLC) and making investments through it is a common approach. An LLC is a legal hybrid that offers the limited liability protection of a corporation while maintaining tax transparency.

An LLC is not a taxable entity itself. Instead, for tax purposes, the income and expenses of the LLC “flow through” to its owners, who report them on their individual or corporate tax returns, depending on their status. If a single individual owns the LLC, it is taxed similarly to a sole proprietorship. However, despite tax transparency, the LLC remains a separate legal entity, limiting the liability of its owners to the amount they have invested in the company.

Despite these advantages, there are potential disadvantages. First, Israeli tax authorities do not automatically recognize the LLC’s tax transparency, which may lead to double taxation or prevent Israeli investors from receiving tax credits for U.S. taxes paid. Second, an LLC does not provide an exemption from U.S. estate tax.

Investing through a C Corporation (C-Corp)

Some investors choose to invest through an American corporation (C-Corp). In this structure, the investment is subject to U.S. corporate tax rates, and because the shares of the company are U.S.-based assets, they may also be subject to U.S. estate tax.

Although the 2018 tax reform reduced the corporate tax rate, the overall tax burden for an individual investor is typically lower than that of a C-Corp. However, a significant advantage of using a C-Corp is that it allows the deduction of certain business expenses, which may reduce the overall tax liability.

Investing through a Foreign Company

Another option is investing through a foreign company (Israeli or otherwise). In this case, the investment is subject to corporate tax regulations and may also be taxed when transferring funds abroad. However, a key advantage of this structure is that it provides an exemption from U.S. estate tax, which can be a significant consideration for long-term investors.

By carefully choosing the appropriate investment structure and incorporating tax planning into your real estate strategy, you can maximize profitability while minimizing tax liabilities. Given the complexities of U.S. and Israeli tax laws, consulting with a US tax advisor in Israel experienced in cross-border real estate investments is strongly recommended.

U.S. Taxation on Real Estate Investments Depending on the form of Investment

* The table does not refer to the applicability of other possible taxes such as the state tax, city tax, etc., but these taxes will inevitably apply as well.

Each of these investment types is taxed differently. We will now turn to examine the differences in taxation.

Taxation of Real Estate Investments – Current Income

American tax law distinguishes not only between the various forms of property ownership (as described above) but also between the different types of income: whether it is current income (reported from rents) or capital gains (profit from the sale of assets).

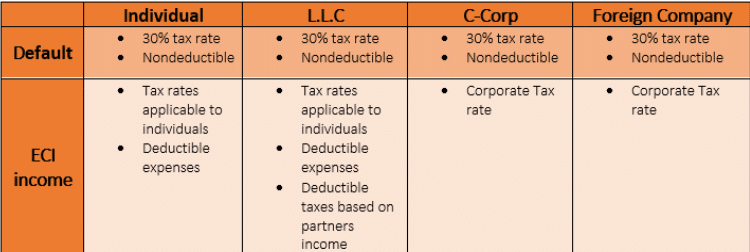

When real estate generates profits from rental income, the investor can choose one of two taxation routes:

- Uniform Tax Rate – Income from rent paid to foreign investors is generally classified as FDAP (Fixed, Determinable, Annual, or Periodical) income, which is taxed at a flat rate of 30%.

- Taxing Rental Receipts as Business Revenue – Rental income can be classified as effectively connected income (ECI), allowing for deductions of rental expenses.

By default, rental income is subject to a 30% tax withholding. Not only is this a high tax rate, but it also does not allow for the deduction of rental expenses.

Proper tax planning can help minimize tax liability by defining rental income as ECI (Effectively Connected Income). This classification allows rental expenses to be deducted, and the tax rates are determined as follows:

- For a private investor or an LLC not owned by a corporation – The income is subject to marginal tax rates applicable to individuals, which range from 10% to 37%, depending on income levels.

- For investments through a corporation (foreign or C-Corp) – Corporate tax rates apply. Following the 2018 tax reform, the corporate tax rate is 21%.

Additionally, there is a potential tax benefit for transparent taxable partnerships such as LLCs. Since the 2018 tax reform’s reduction of corporate tax rates does not apply to LLCs (which are treated as pass-through entities for tax purposes), the reform introduced a tax deduction of 20% on LLC revenues.

An LLC whose income is classified as business income, and whose partners’ combined annual revenue does not exceed $315,000, is eligible for a 20% deduction on that income. If the partnership’s income exceeds this threshold, the deduction is limited to the lower of the following:

- 50% of the total wages paid to the partnership’s employees.

- 25% of wages paid plus 2.5% of the cost of depreciable assets for U.S. taxation purposes.

Tax rates applicable to current income from real estate businesses

Taxation of Real Estate Investments – Profit from Selling a Property

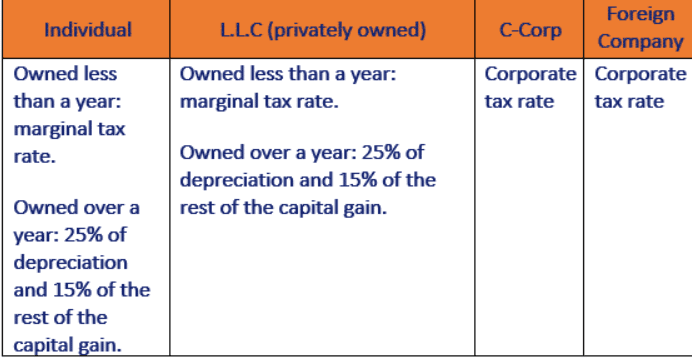

As mentioned earlier, real estate can generate profits not only from rental income but also from the sale of a property, known as a capital gain. The taxation of capital gains depends on the holding period of the property and the investment structure.

- For corporate investments – Capital gains on real estate held by a company, whether local or foreign, are taxed at the corporate tax rates applicable to companies. The same applies to an LLC owned by a local or foreign company.

- For individual or non-corporate LLC investments – Capital gains are taxed at the marginal tax rates applicable to individuals. If the property has been held by the same investor for more than one year, long-term capital gains tax rates apply, which are lower:

- The gain attributed to depreciation recapture is taxed at 25%.

- The remaining profit is taxed at 15%.

This applies as long as the profit is classified as capital gain and not ordinary income, which is taxed according to the rules detailed above.

Additionally, when dealing with capital gains from real estate, investors may have the option to defer capital gains tax through an exchange procedure, such as a 1031 exchange. This allows for tax deferral if the proceeds from the sale are reinvested in a similar property within a specified timeframe.

Taxation on capital gain income

Estate Tax

An estate tax is a tax imposed on the transfer of a person’s assets upon their death. In the United States, the estate tax is widely applicable and has one of the highest rates in the world. As a result, not only are American citizens subject to this tax, but foreign nationals as well. The estate tax applies to any individual—regardless of citizenship—who, at the time of their death, held assets in the United States exceeding $60,000 in value. This tax can reach rates of up to 35%, an exceptionally high percentage by all standards.

The potential financial impact of this tax is significant. Even an Israeli citizen who owns real estate in the United States is subject to it and could lose a substantial portion of their investment. Therefore, professional tax planning is essential to tailor solutions that minimize tax liability.

While real estate investments offer considerable benefits, they also involve financial risks due to estate tax—whether the investment is made directly as an individual or through an LLC. In such cases, the assets will be considered as located within the United States and will be taxed accordingly.

However, since shares of a foreign company are considered assets located outside the United States, they are not subject to U.S. estate tax. Consequently, upon an investor’s death, their assets held through a foreign company will not be taxed under estate tax laws. Despite this advantage, there are also drawbacks to investing through a foreign company. A foreign company is subject to corporate tax rates, which are often higher than individual marginal tax rates. Additionally, a foreign company does not benefit from lower capital gains tax rates and may be subject to branch tax when transferring profits from the United States, as well as Israeli dividend tax when distributing funds to an Israeli investor.

How Can These Issues Be Addressed?

In some cases, structuring investments through a foreign trust or life insurance policy may provide an advantage. However, the best approach depends on the specific circumstances of the investor and their investment. We are available to assist you in determining the optimal solution for your needs.

Branch Tax

The branch tax applies to foreign companies seeking to withdraw profits from their U.S. operations. For example, when an Israeli company operating in the United States wishes to distribute profits as dividends, it must pay not only corporate tax but also branch tax.

The branch tax is imposed on revenue after deducting corporate taxes. Its standard rate is 30%, but under the tax treaty between Israel and the United States, this rate has been reduced to 12.5%.

Branch tax can sometimes be avoided by reinvesting profits or by structuring transactions as loans from the foreign company to an LLC owned by the investor. Additionally, the tax is not imposed in the year the company ceases operations, meaning that liquidation of the company can eliminate the tax obligation.

Income Tax in Israel on Real Estate Investments in the United States

An Israeli citizen investing in U.S. real estate is subject to taxation both in the United States, where the income is generated, and in Israel. First, taxes are paid in the United States, followed by taxation in Israel. Therefore, obtaining credit for foreign taxes paid in the United States is crucial.

The Israeli Income Tax Ordinance provides that an Israeli resident may receive a credit for “foreign taxes” paid on income earned abroad. However, without professional tax planning, complexities may arise, potentially resulting in double taxation.

Investing as an Individual

For individuals, taxation is relatively straightforward. Investors may choose between two taxation methods:

- Marginal Tax Rate – Income is taxed at the individual’s marginal tax rate, based on total income. Under this method, the investor can deduct expenses and receive a tax credit for taxes paid in the United States.

- Fixed Tax Rate – Income is taxed at a flat rate of 15%, without the ability to deduct expenses or claim a tax credit for foreign taxes.

Investing as a C-Corp

For investors using a C-Corporation, taxation follows a two-step system:

- The corporation itself is taxed on its profits.

- When profits are distributed to Israeli shareholders, additional taxes apply.

Investing Through an LLC

Investing through an LLC presents unique complexities.

As noted earlier, U.S. law treats LLCs as pass-through entities for tax purposes, meaning the owners are taxed directly on the company’s income. However, Israeli tax law does not recognize this classification. Instead, it considers an LLC a regular corporation, leading to double taxation:

- In the United States, the LLC’s owners are taxed as individuals.

- In Israel, the LLC is taxed as a corporation, with profits taxed only upon distribution to Israeli residents. However, Israeli investors cannot receive credit for taxes paid in the United States.

For years, this issue remained unclear, but in the last few years, two key court rulings have attempted to resolve the asymmetry between U.S. and Israeli tax laws. The Israeli courts upheld the Tax Authority’s position that LLCs are corporations for Israeli tax purposes. As a result, taxpayers earning income through LLCs have two options:

- Classify the LLC as “Opaque” – The company is taxed only upon dividend distribution. However, under this option, investors cannot offset U.S. taxes against Israeli dividend tax liability.

- Classify the LLC as “Transparent” – The investor is taxed on the company’s income but can offset U.S. taxes paid. No additional tax is imposed when distributing dividends.

The court also ruled that multiple LLCs owned by the same taxpayer cannot offset profits and losses between them.

Despite these rulings, many uncertainties remain. Given this lack of clarity, comprehensive and professional tax planning is essential.

Summary

Investing in U.S. real estate has become increasingly attractive and is no longer limited to major investors. Due to relatively low real estate prices, investment opportunities are abundant. However, careful consideration of tax implications is essential.

This article only scratches the surface of U.S. taxation and foreign real estate investments. The complexities of U.S. tax law include thousands of provisions and regulations. Navigating these rules requires extensive knowledge and expertise. Without proper tax planning, investors risk losing tens or even hundreds of thousands of dollars, significantly impacting the profitability of their investments.

When it comes to U.S. real estate investments, comprehensive tax planning is essential.

Our team of experts is well-versed in all aspects of American taxation. We are here to guide you and provide tailored solutions to meet your investment needs.